Hedging And Bitcoin Mining Risk Management

Hedging in Bitcoin Mining for Sustainable Profitability

By Dan Rosen

Over the years, as businesses have become more sophisticated in their operations, so too have their budgeting, risk management, financial analysis, and hedging strategies. Locking in revenues and commodity input costs through hedging has enabled these companies to plan operations more efficiently into the future and ensure sustainability and profitability.

Specifically, in the Bitcoin mining business, Bitcoin miners can now do the same. Miners are in the business of arbitrage - they aim to secure low energy input costs and high value Bitcoin outputs. These days, both the inputs (electricity) and the outputs (hashrate) can be hedged well ahead of time, enabling miners to budget and manage risk efficiently.

History of Hedging, Agriculture, and Chicago

Farmers have sold their crops at the market for thousands of years, but they had long been at the mercy of the market, depending on who showed up to the market that day to buy their crops and how much they wanted to buy.

Although the Dojima Rice Exchange in Osaka, Japan, in 1697 was perhaps the first commodities exchange to be established, Chicago’s Board of Trade became well-known for being the first exchange to offer a variety of commodities in 1848 - wheat, corn, cattle, and other livestock. In the mid-1800s, Chicago became a hub for Midwest farmers to come and sell their grain to dealers who would then send the grain across the U.S. by rail. However, while farmers got paid for their crops, there was no certainty that they could sell their entire crop at a reasonable price.

Farmers competed against each other to sell their crops at lower and lower prices to dealers; if they could not sell their crop at the market, they could use it to feed their animals - otherwise, it was wasted. Dealers were also at risk in the event of a particularly poor harvest - prices could be sky-high given the limited amount of crops available to purchase.

The Critical Role of Hedging

Rather than farmers and dealers continuing to take the risk of uncertainty of price and quantity available, they began to enter contracts ahead of time, with dealers committing to buy a specific quantity of grain from farmers at a previously agreed-upon price. Knowing they had secured a supply of grain at an agreeable price allowed dealers to turn around and enter contracts with their own customers ahead of time.

Farmers, on the other hand, had price assurances for their crops, without having to take the risk that prices would decrease in the time between when they planted their crops and after the harvest when they sold their crops.

These contracts brought stability to the system, allowing dealers to budget and run their businesses profitably and farmers to reduce waste and plan for the harvest. Eventually, these contracts became standardized, and exchanges proliferated across the world in Chicago, New York, London, Amsterdam, Tokyo, and more, trading everything from coffee, cotton, copper, lead, zinc, butter, and eggs to foreign currencies, interest rates, oil, natural gas, equities, and treasuries.

Hedging Today

Nowadays, hedging and managing risk has become a normalized and integral part of all companies, especially for those dealing with commodities in their normal course of business.

For example, airlines buy jet fuel to operate their business and thus are exposed to jet fuel’s market price. To hedge their exposure to increased jet fuel prices, airlines enter into forward contracts where two parties agree to buy and sell a quantity of jet fuel at a specified price on a future date. These types of contracts allow airlines to budget proactively, as they know the exact price of one of their business input costs ahead of time.

On the other side of the forward contract, you’d expect to see jet fuel producers - Exxon Mobil, Shell, BP, Chevron, etc - locking in a price in the future at which they are willing to sell their jet fuel production. These types of forwards contracts typically are private, fully-customizable agreements traded OTC (Over-The-Counter).

In contrast, commodity futures contracts are standardized and traded on exchanges such as CME Group, the London Metal Exchange, and Intercontinental Exchange (ICE). The type of venue and contract terms can vary significantly depending on the underlying commodity, geographic location, and counterparties’ needs.

Similar markets and contracts exist in virtually every commodity, allowing buyers and sellers to lock in costs or revenue ahead of time.

Bitcoin Hashrate: Commoditizing the Backbone of Bitcoin Mining

The definition of a commodity (per Wikipedia) is “an economic good, usually a resource, that specifically has full or substantial fungibility: that is, the market treats instances of the good as equivalent or nearly so with no regard to who produced them.”

Without diving into Ordinals and ordinal theory, Bitcoin hashrate, and the associated Bitcoin rewards are fully fungible, and users of the network don’t care whether Marathon, Riot, Cleanspark, or Cipher mined the Bitcoin on Foundry, Antpool, F2Pool, or Luxor Mining Pool. Bitcoin network hashrate is undifferentiated from one miner to another and is typically sold to pools in exchange for Bitcoin. Further proof lies in the numbers; there are currently somewhere in the neighborhood of 6 million ASICs combining for a network hashrate of 535 EH.

Hedging in Bitcoin Mining: Power, Hashprice, and Treasury

Bitcoin miners are exposed to three primary risks: power, hashprice, and treasury. The first of these risks - power/electricity - is the primary input to mining (other than the ASICs themselves). Many miners have fixed contracts for purchasing electricity, whether in the form of a PPA (power purchase agreement) with a power generator or an agreement with a hosting facility. While some agreements may allow for a floating price, the majority of these agreements have a fixed price so that the miner knows their exact cost of hashrate production.

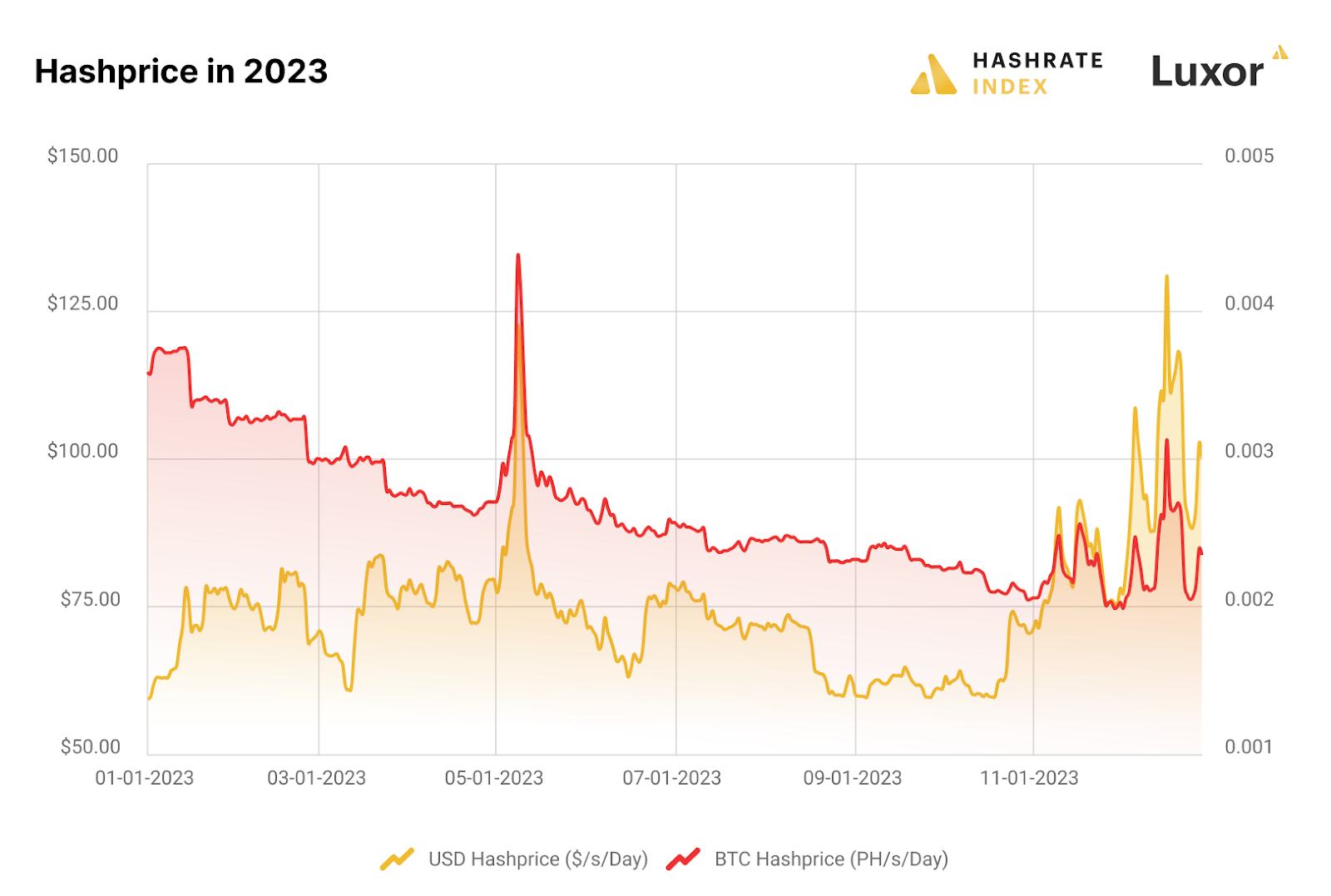

The second of these risks is the revenue the miner generates from their production of hashrate. Earlier, we noted that the majority of miners sell their hashrate to pools, who in turn consolidate the hashrate to minimize the risk for individual miners, preventing them from covering electricity expenses without successfully discovering a block. By receiving these payments for hashrate, miners are able to reduce volatility in their revenue and smooth out their daily rewards. The value of this hashrate and the revenue the miner generates can be quantified, and it is frequently referred to as hashprice. Hashprice is often quoted as 1 PH of hashrate per second per day on the Bitcoin network. As of publication, 1 PH is worth approximately 0.00205 BTC/s/Day, or $92.75 USD/s/Day if converted to USD using Bitcoin price.

Hashprice, in BTC terms, comprises three components - the block subsidy (currently 6.25 BTC per block), transaction fees, and network difficulty. The first two components - the block subsidy and transaction fees - positively correlate to hashprice. As the block subsidy and transaction fees decrease, so does hashprice (and vice versa). However, network difficulty, the third component, is negatively correlated to hashprice; as network difficulty increases, hashprice decreases. Intuitively, this makes sense - as more hashrate comes online, network difficulty increases with more hashrate chasing the same block reward.

Hashprice in USD terms simply converts the BTC hashprice using the USD price of Bitcoin. USD-denominated hashprice will thus be significantly more volatile by adding Bitcoin price as the 4th component to the mix.

The third of these risks for miners is holding Bitcoin on the balance sheet or in treasury. Given that Bitcoin miners’ liabilities are almost entirely denominated in a fiat currency such as USD, there is a significant exchange price risk to holding Bitcoin on the balance sheet. As we saw most recently in 2022, miners who continued holding large amounts of Bitcoin on their balance sheet without hedging suffered. Bitcoin price dropped by over 75% in USD terms, and their liabilities and expenses for electricity bills, equipment costs, and employee salaries, and debt were denominated in USD or other fiat currencies. This mismatch of assets and liabilities caused many miners to suffer and several to file for bankruptcy or go out of business entirely.

The risk of holding Bitcoin on your balance sheet can be minimized in several ways. First, if the profit margin for mining is large enough, then there is relatively little concern about being able to pay your bills. Second, derivatives can be used to hedge USD price exposure to BTC by selling futures, call options, or buying put options. Third, miners typically sell either a percentage of or their entire production of Bitcoin on the spot market to receive USD in exchange for the Bitcoin. The amount of Bitcoin that each miner wants to or should sell for fiat is dependent on its individual situation - electricity costs, equipment costs, salaries, debt, etc.

The Necessity of Hashrate Hedging in Bitcoin Mining

Suppose hashrate on the Bitcoin network is a commodity, and commodity producers in every mature and established industry hedge a portion of their production. Shouldn’t Bitcoin miners hedge their production, too? Emphatically - yes!

As discussed, hashprice (the expected revenue for 1 PH of hashrate) is affected by transaction fees and network difficulty. As the total hashrate on the network increases over time, the value of a hash decreases, and more competition for the same reward leads to a lower hashprice.

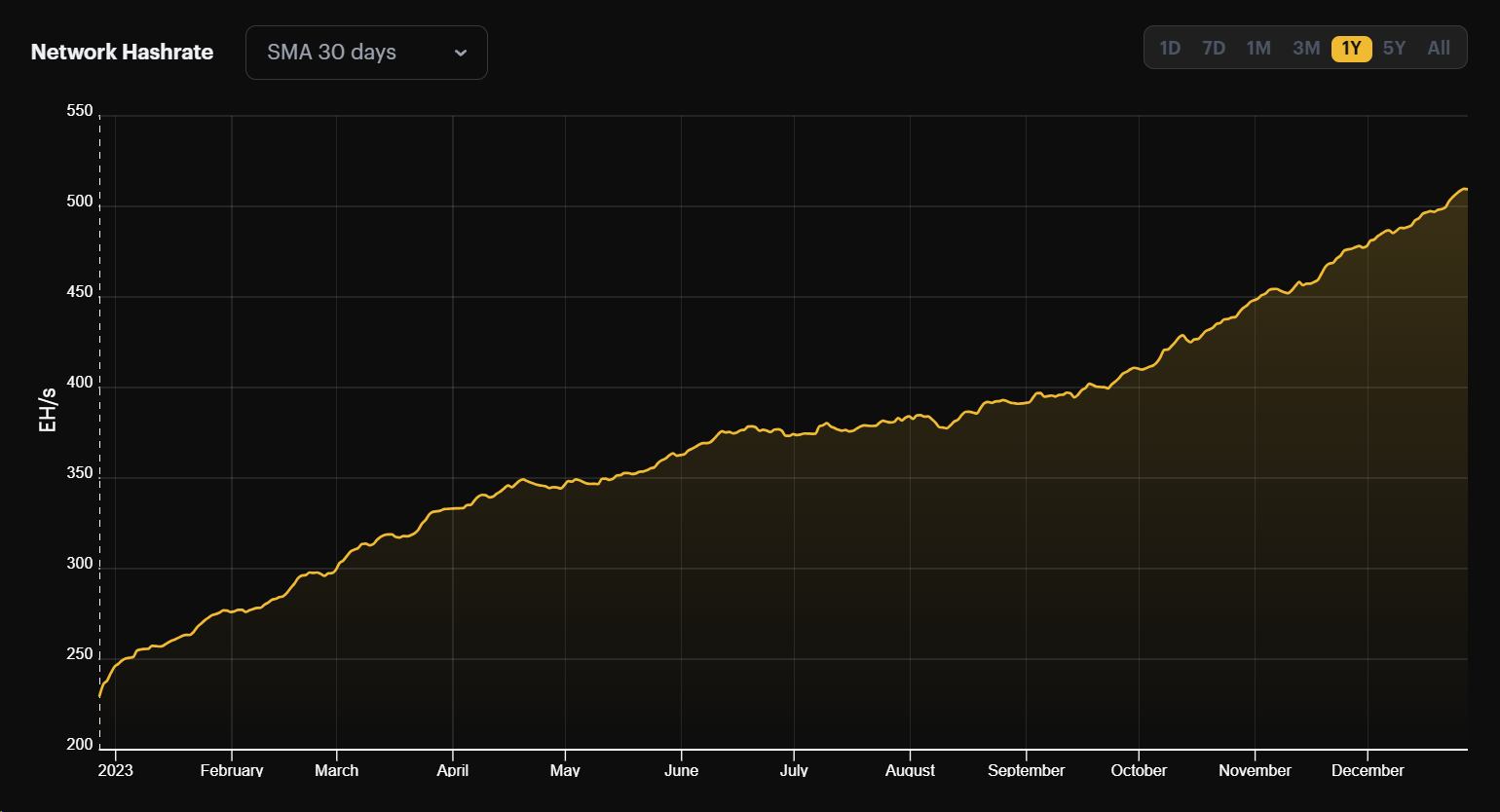

This uncertainty makes it difficult for Bitcoin miners to budget and plan for revenues. If you don’t know how much Bitcoin you will receive in revenue for your 500 PH of hashrate in 3 months from now or 6 months from now, how can you accurately plan for expansion? Network hashrate at the beginning of 2023 was at ~250 EH; I’m doubtful that many miners on Jan 1 expected network hashrate to end the year anywhere near the current ~530 EH. So, this is the risk - if network hashrate and associated mining difficulty rise faster than a miner expects, then the miner’s revenue will be lower.

Fortunately, miners can hedge this exposure using hashrate forwards to lock in a set revenue per PH for up to 6 months in advance. Miners, as producers of hashrate, are naturally long hashprice; as hashprice increases, so does their revenue. However, the opposite is also true - as hashprice decreases, so does their revenue. To hedge their long hashprice exposure, miners would be sellers of hashprice in the marketplace.

Practical Hedging Strategies for Bitcoin Mining Firms

Every miner’s operations are unique, and no one hedging solution fits all miners. From distinctive PPAs to unique hosting agreements to specialized revenue or profit splits, every situation has to be analyzed before tailoring a hedging strategy to a particular miner.

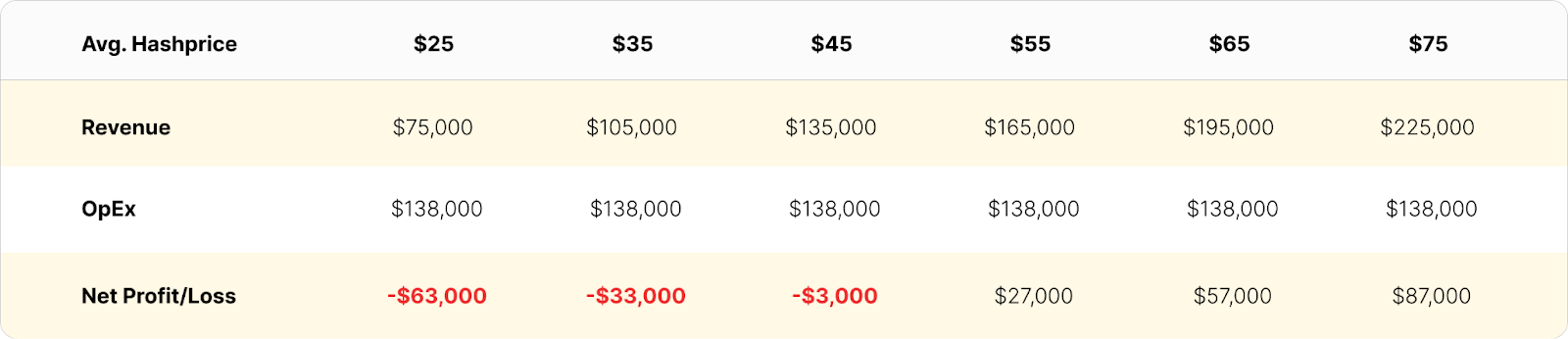

However, as a generalization, many miners like to lock in revenues that will, at a minimum, cover their operating expenses. So, let’s look at an example of a miner with the following profile looking to hedge hash price for the next month to ensure they can cover OpEx.

Assumptions:

- Hashrate: 100 PH

- Duration: 30 Days

- Fleet Efficiency: 30J/TH

- Electricity Costs: $0.05/kWh

- Monthly OpEx: $108,000 electricity + $30,000 in SG&A = $138,000 total

First, let’s look at a range of hashprices to understand how profitable the operation is and where the breakeven point is:

This mining operation breaks even around $46 hashprice, and the difference in monthly profit between $55 and $75 hashprice is significant.

Next, let’s look at a miner who hedges 50% of their hashrate by selling hashprice at $75 for 30 days. The hedge ensures they will receive a minimum of $112,500 for the month ($75 x 30 days x 50 PH) regardless of where hashprice goes, and we can see that the hedge considerably stabilizes their revenue.

While this latest chart shows the potential downside in hashprice, many miners don’t want to lose out on the upside in hashprice. Let’s look at what the upside in hashprice looks like, even with a 50% hashrate hedge in place.

The 50% hedge in the examples above shows that the miner’s exposure to the downside in hashprice does not significantly hinder their ability to capture upside should transaction fees or Bitcoin price rip higher. A proper hedge ensures that a commodity producer remains operational and in business regardless of market conditions.

Forecasting and Future-Proofing in Bitcoin Mining through Hedging

There is a reason that virtually every mature commodity business engages in hedging - to demonstrate to its owners and shareholders that it plans on being around next month, the following month, and next year. Ultimately, a miner is in the business of energy arbitrage; its profit margin is the difference between the revenue it receives for its hashrate and its costs of producing that hashrate. By locking in a percentage of that revenue by hedging, the miner responsibly guarantees that a part of its fleet will be profitable.

With the halving around the corner in April 2024, we can expect profit margins to shrink from current levels, and the importance of locking in these smaller margins will only continue to grow.

Disclaimer

This content is for informational purposes only, you should not construe any such information or other material as legal, investment, financial, or other advice. Nothing contained in our content constitutes a solicitation, recommendation, endorsement, or offer by Luxor or any of Luxor’s employees to buy or sell any derivatives or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the derivatives laws of such jurisdiction.