Hashprice At All Time Lows: How Can Miners Use The Forward Curve?

This is article is syndicated from an original on Hashrate Index.

Hashprice has plummeted to an all-time low. On August 5, Bitcoin miners faced a perfect storm: a global asset sell-off paired with a steep decline in Bitcoin prices, a significant and unexpected mid-summer increase in mining difficulty, and a stagnant transaction fee market. Hashprice settled at $37.70 per PH/s/Day.

In response to these daunting challenges, miners are faced with pivotal decisions. They must consider whether to hedge their hashprice risk to protect mining margins, seize the opportunity to buy more hashrate at lower prices, or in a worst-case scenario, shut down their ASICs and explore alternative revenue streams.

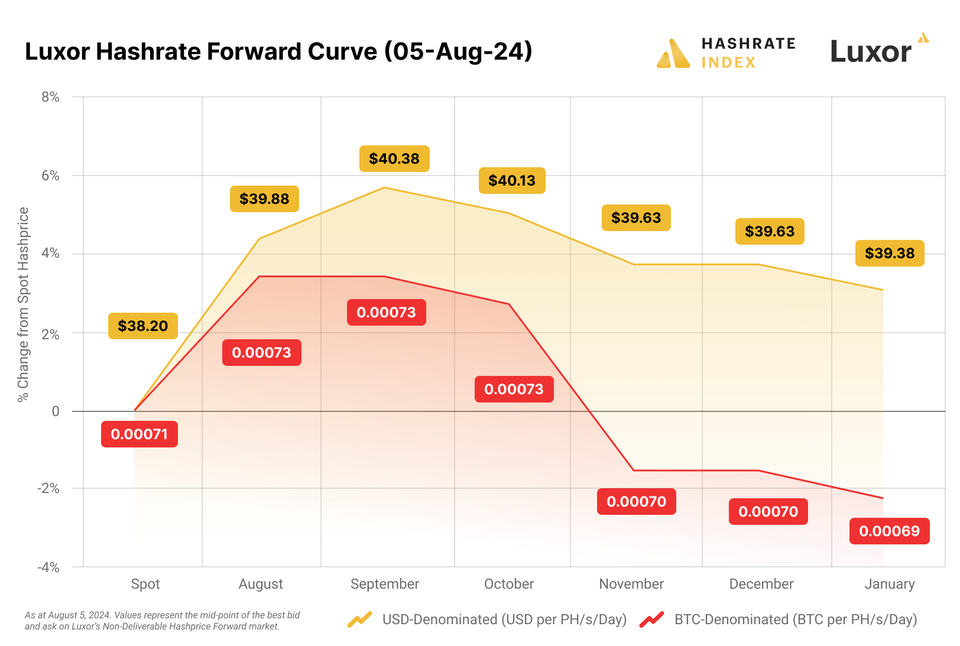

As the market shifts, the strategy miners choose will significantly impact their future. Fortunately, miners can now use Luxor’s Hashrate Forward Curve to manage risk and capitalize on market opportunities. Here's the case for buying or selling forward hashrate at these all time low levels.

The Case For Selling Hashrate Forward

The case for selling forward at current levels is straightforward. Although hashprice is at all-time lows, that does not mean it won’t go even lower. Another 20% decline in Bitcoin prices (which is not outside historical precedent) and we are in the 20's for hashprice. In such a situation, hedging hashprice could literally save a mining business and keep electricity flowing through a bear market. At this hashprice, unhedged miners are risking their business on unpredictable market movements.

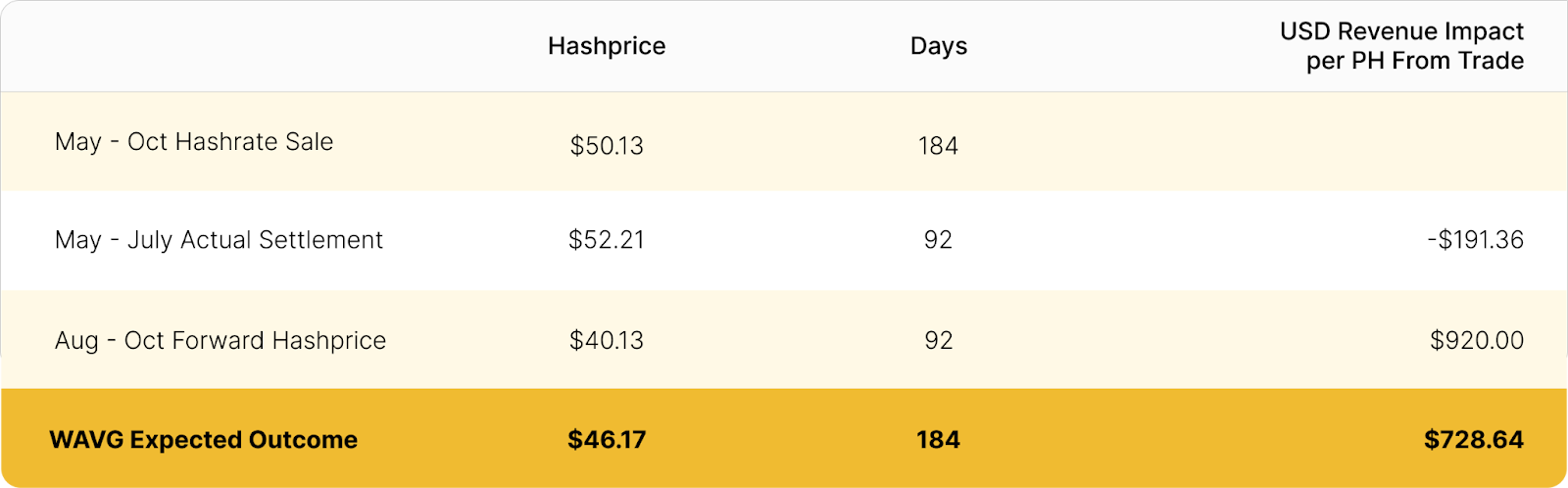

As an illustration, take a look at how miners that hedged post-halving performed, when hashprice was at a previous all-time low. In late April / early May, miners using Luxor’s Hashrate Forwards were able to lock in an average hashprice of $50.13 from May - October 2024. For the first half of the contract, the hedge cost the miner $191/PH, since hashprice settled slightly higher at $52.21. Today, that same miner could close out the remaining 92 days of their contract at $40.13 for a gain of $920/PH. For a 1 EH mining operation, that is nearly one million dollars added to projected revenue over the period.

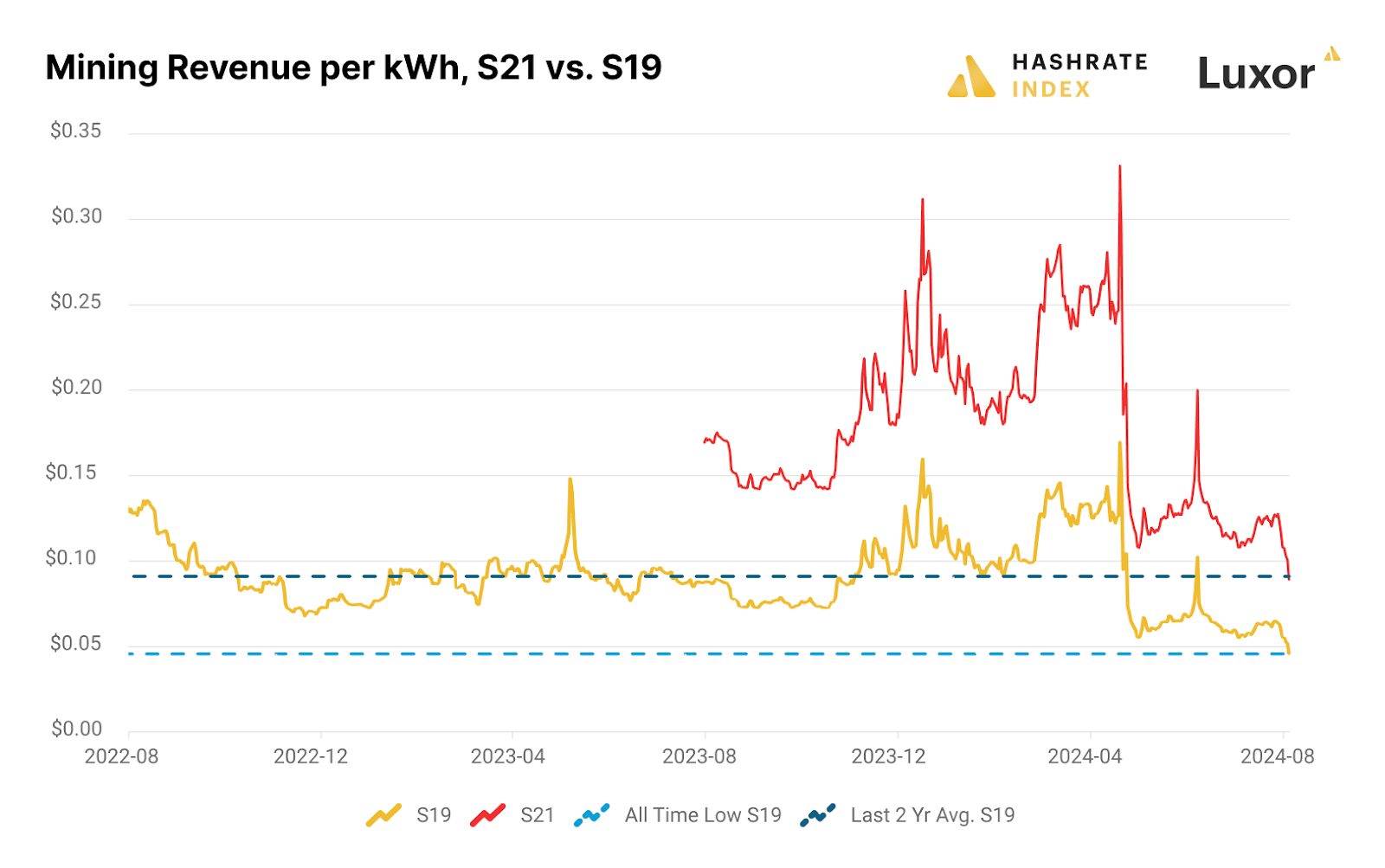

It is also important to remember that while miners are earning an all-time low per hash, newer generation miners are not earning an all-time low per unit of electricity. On a kWh basis, S21 Bitcoin miners can hedge their hashrate production for six months at approximately $0.09-0.10 per kWh. This revenue is in line with the average S19 hashprice per kWh over the last two years, 95% higher than today’s all time lows for the S19, and 31% higher than the S19 post-FTX collapse. All this to say – even at all time lows, there is meaningful margin for newer generation ASIC operators to lock in!

The Case For Buying More Hashrate

For risk-takers in the Bitcoin mining game, snagging hashrate at rock-bottom prices could be a smart move, especially if you time it right. If you think the hashprice will climb — maybe because Bitcoin’s price bounces back, mining difficulty drops as miners drop off the network, or transaction fees jump — buying forward hashrate now is the most efficient, cost-effective way to boost your mining revenue. Plus, it’s cheaper than ever. And if you're dealing with outdated gear or high electricity costs pushing your "hashcost" [1] over the forward curve, then picking up hashrate straight from the forward curve can immediately cut your cost to acquire Bitcoin.

We have the tools and markets to help meet your production targets.

Footnotes

- Hashcost = $/kWh * j/TH * 24

Disclaimer

This content is for informational purposes only, you should not construe any such information or other material as legal, investment, financial, or other advice. Nothing contained in our content constitutes a solicitation, recommendation, endorsement, or offer by Luxor or any of Luxor’s employees to buy or sell any derivatives or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the derivatives laws of such jurisdiction.