Evaluating Luxor’s Hashprice NDF with Historical Data

What the Last Five Years of Data Tells Us About Luxor's Hashprice NDF

By: Ben Harper

Evaluating a New Product with Historical Data

Just over a month ago, Luxor launched the Bitcoin Hashprice Non-Deliverable Forward (NDF). It has generated interest from miners and hosting sites looking to hedge their revenue, investors who want non-physical exposure to hashrate, and financiers looking to hedge counterparty risk on their loan book.

For all market participants, historical performance and NDF contract outcomes are top of mind. Unfortunately, with only one month passed since the NDF launch, there isn’t enough data to properly evaluate the contract over an extended period of time. For this reason, to give market participants a true gauge of NDF behavior, we must turn to historical data and evaluate what would have happened before the NDF launched, not just what did happen over the last month.

Recap: What is Luxor’s Hashprice NDF?

A forward contract is made between two parties. It typically has one of two outcomes: physical delivery or cash settlement. In a physically delivered contract, one party agrees to buy a commodity on a future date, at a fixed price. The other party agrees to deliver that commodity or asset on the future date, at that fixed price. In a non-deliverable, cash-settled forward contract (NDF), the difference between the fixed price of the contract and the settlement value of the underlying commodity at the expiration of the contract is paid in cash from one party to the other.

Luxor’s Hashprice NDF brings together buyers and sellers of hashrate for customizable, non-deliverable hashprice forwards. After completing the appropriate onboarding documentation, the buyer and seller of a Luxor NDF contract simply agree to the following:

- Unit Hashprice (e.g., $80.00 per PH/s/Day)

- Daily Hashrate (e.g., 30 PH/s)

- Duration (e.g., 90 days)

Luxor facilitates the contract by matching counterparties, promoting price discovery, managing counterparty risk, providing tools for daily profit and loss calculation, and acting as the settlement agent (the contract is settled to Luxor’s Bitcoin Hashprice Index).

There are a couple nuances to keep in mind when evaluating NDF performance using historical data.

First, the unit hashprice is settled against the average hashprice through the duration of the contract to account for the fact hashrate is a continuously delivered commodity (like electricity). This stands in contrast to a discreetly delivered commodity (like corn or oil), which would instead settle against the final market value of the commodity at the end of the contract. This averaging mutes the volatility of Luxor’s NDF contract.

Second, we must evaluate historical performance and outcomes relative to a fixed anchor.

That’s easy for a real Hashprice NDF contract. We look at the difference between the unit hashprice and the final settlement rate (i.e., average hashprice through the duration of the contract). If the final settlement rate is higher than the unit hashprice, the seller pays the difference to the buyer. If the final settlement rate is lower than the unit hashprice, the buyer pays the difference to the seller.

However, when looking at hypothetical contracts on historical data we don’t have an actual unit hashprice that a buyer and seller agreed upon. So for this analysis, we will compare contract settlement rates to daily average hashprice one-day prior to the NDF start date. While imperfect, this will give a sense of NDF outcomes relative to hashprice at the beginning of the contract.

Please keep in mind that actual returns will be relative to pre-agreed unit hashprice, which could be above or below hashprice at the beginning of the contract. For reference, during the first month of trading, 30-day contracts have traded from a 0.1% premium to a 4.5% discount from average hashprice the day prior.

Hypothetical Hashprice NDF Outcomes by Duration

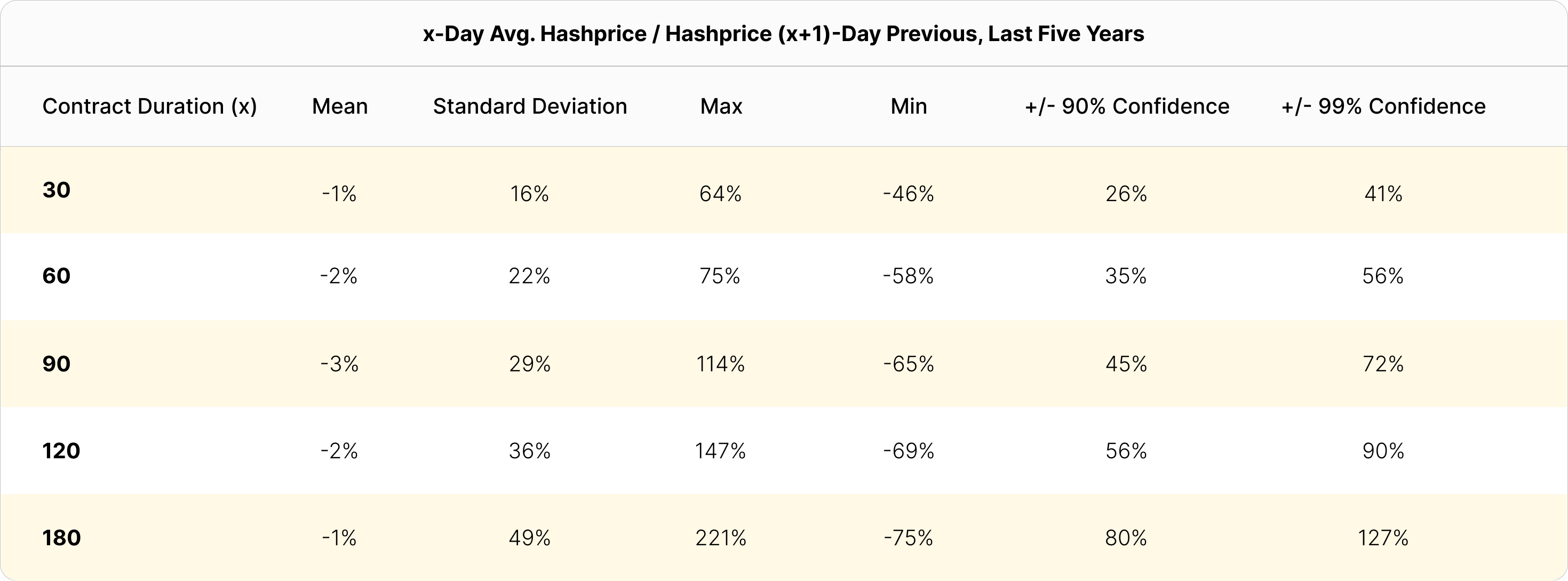

For robust data on historical NDF performance, we evaluated 30, 60, 90, 120 and 180-day contracts over the past five year period. For each contract duration, and for each day in the period, we evaluated how a hypothetical contract would have settled relative to the average hashprice one-day prior to the trade. For the five year-period, this gives us a sample size equal to 1,827 (the number of days) less the contract duration (because the first contract cannot close until the duration has lapsed).

This first chart shows USD hashprice.

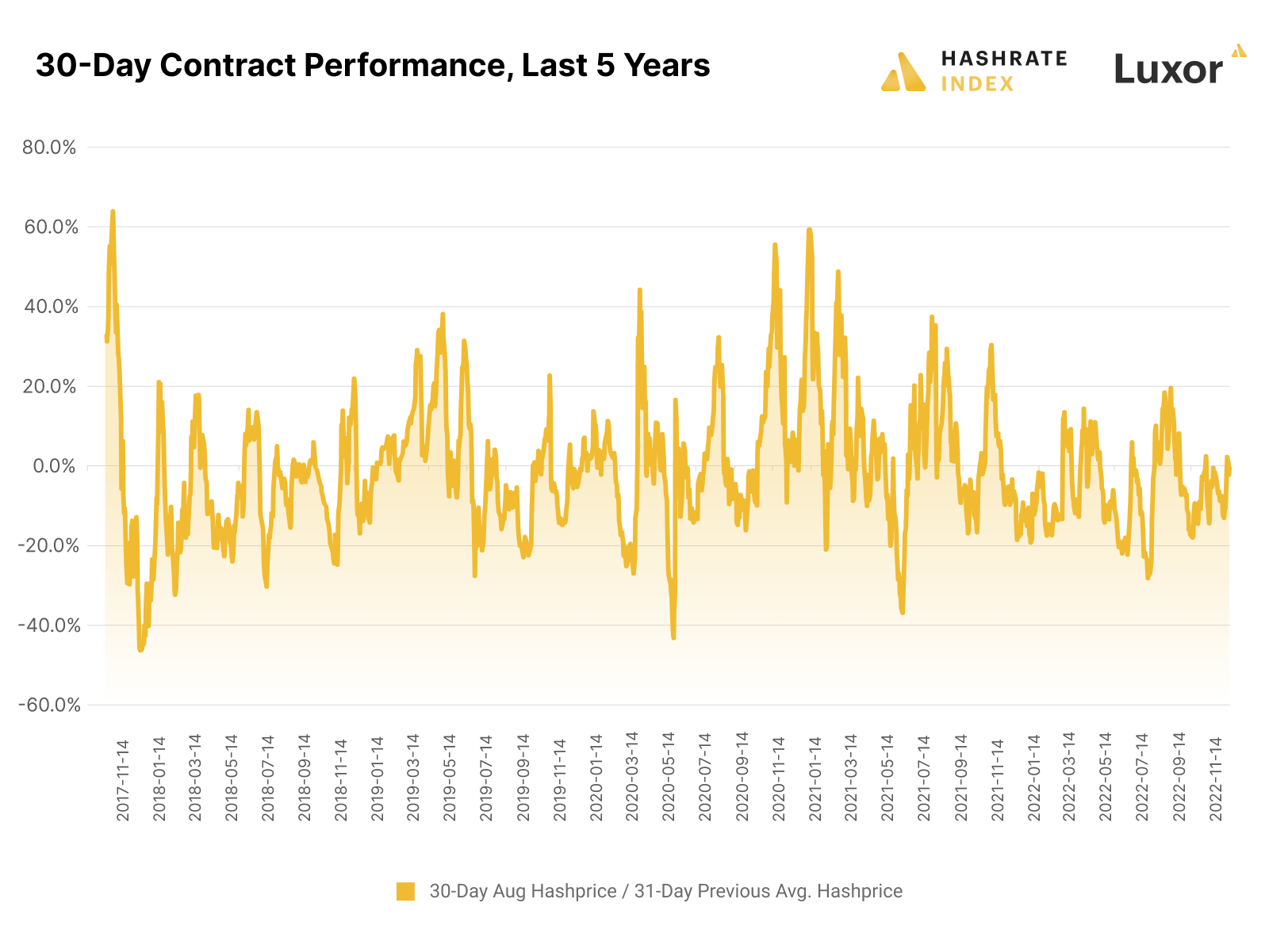

The next two charts show the calculation described above for hypothetical 30-day contracts over the last five years. The first shows the performance across time and the second shows the frequency of different outcomes in a histogram. These charts show how 30-day NDF contracts would have settled every day over the last five years relative to hashprice 31 days prior. When the number is positive, the seller would have paid the difference to the buyer, and when the number is negative, the buyer would have paid the difference to the seller. The performance of the contract is shown below on a percentage basis – actual payouts would have been proportionate to the size of the contract (i.e., daily hashrate under contract).

The table below summarizes the data for 30-day contracts and also includes summary statistics for 60, 90, 120, and 180-day NDFs. The first column indicates the contract duration being analyzed. The next four columns show the mean, standard deviation, maximum and minimum outcomes for each contract duration over the five year period. The final two columns show confidence intervals, assuming a normal distribution with observed mean and standard deviation over the last five years.

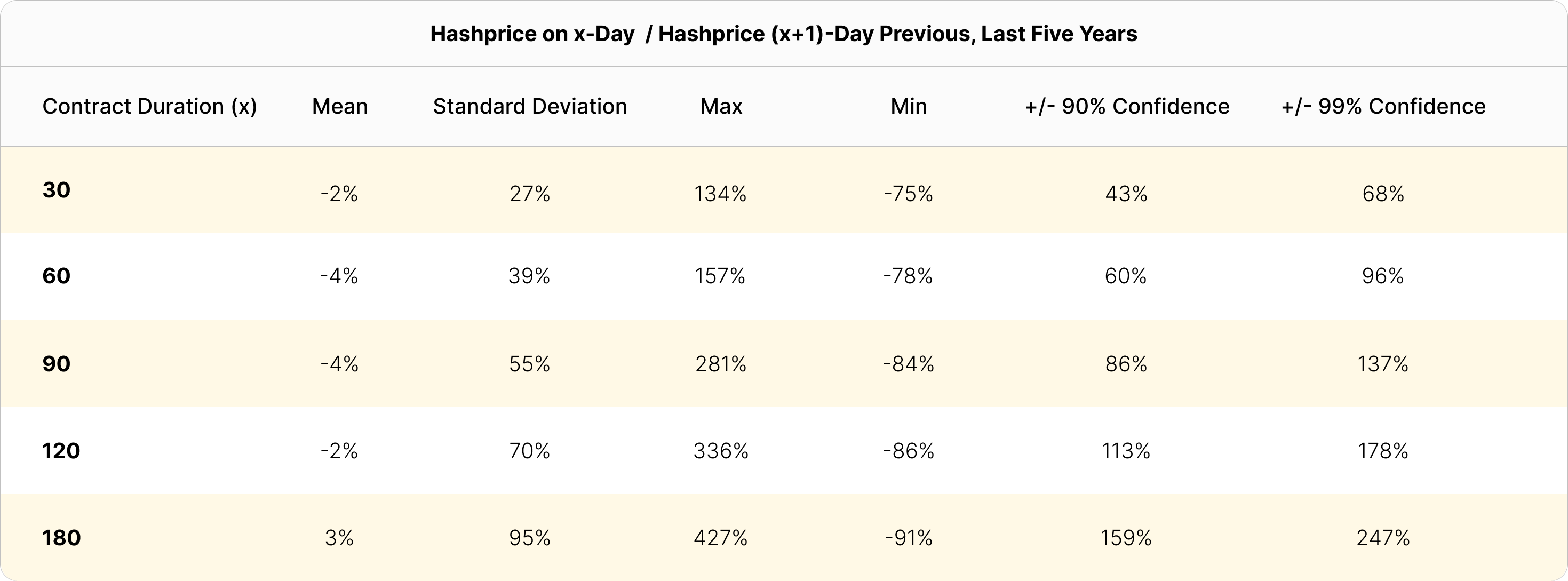

To illustrate how averaging mutes the volatility of the hashprice NDF, we ran the same analysis in the chart below, but with hashprice on the last day of the contract settled to hashprice the day prior to the trade (i.e., not averaging). The standard deviation, maximum, minimum, and confidence interval values of all contract durations are all significantly higher than when the averaging methodology is used for settlement.

Insights From Historical Data

There are a number of takeaways from this analysis. In particular:

- We observe, on average, a negative trend in hashprice. This is due primarily to increases in network difficulty responding to increases in network hashrate from technological improvements in computing hardware over time (i.e., Moore's Law).

- The volatility of Luxor’s Hashprice NDF increases with duration. This can be observed in the standard deviation, maximum, minimum, and confidence interval columns which are strictly increasing on an absolute basis with duration.

- For all contract durations, the observed maximum outcome is higher on an absolute basis than the observed minimum outcome over the past five years. This is often the case in other derivative markets. Since prices can only fall 100%, buy-side losses are bounded by 100% of the contract value. Sell-side losses on the other hand are unbounded – prices can rise more than 100% and have done so in hashrate markets over the last five years.

- The averaging methodology used to settle Luxor’s Hashprice NDF reduces volatility relative to the methodology used for forward contracts of discrete commodities. This means Luxor’s Hashprice NDF is not only a better hedging instrument than existing Bitcoin futures from a revenue correlation perspective, but has the potential to offer miner’s access to hedging products with lower upfront collateral requirements. This is particularly relevant at a time when Bitcoin mining economics are poor and miners are strapped for capital.

Contact Us

Want to learn more or see the trading desk? Please visit Luxor's derivatives page.

Disclaimer

This content is for informational purposes only, you should not construe any such information or other material as legal, investment, financial, or other advice. Nothing contained on our content constitutes a solicitation, recommendation, endorsement, or offer by Luxor or any of Luxor’s employees to buy or sell any derivatives or other financial instruments in this or in in any other jurisdiction in which such solicitation or offer would be unlawful under the derivatives laws of such jurisdiction.

There are risks associated with trading derivatives. Trading in derivatives involves risk of loss, loss of principal is possible.